In-Field Crude Oil Upgrading, 2026–2030: Monetizing Hard-to-Recover Reserves and Civilian Diversification of the Defense-Industrial Complex

16.02.2026

258

Object of Analysis: Deep hydroprocessing technologies in the context of ensuring macroeconomic sovereignty, utilizing capacities of the Defense-Industrial Complex (DIC), and reproducing the mineral resource base.

Article Authors

Tretyakov A.V. and Tretyakov Y.A.

Table of Contents

CHAPTER I. Macroeconomic Context: Oil in the System of the Sixth Technological Paradigm

In the paradigm of shifting technological waves, modern oil refining is objectively transitioning from the stage of extensive resource combustion to the stage of residue-free molecular design.

- The "Heavy Legacy" Problem: The traditional refinery model, relying on thermal cracking and coking, is strategically exhausted. It generates up to 30% of low-margin fuel oil and petroleum coke, which, under strict environmental regulations (including IMO 2020 standards), turns corporate raw material assets into an economic burden.

- Hydrogen as a Universal Equivalent: Technologies based on hydrogen addition (Hydrogen Addition) allow breaking the historical dependence between the quality of extracted oil and the characteristics of the marketable product. This is a fundamental shift: process economics ceases to depend on the geological features of a specific field, shifting the center of value creation to the high-tech engineering segment.

CHAPTER II. In-Depth Technical Analysis (Genoil GHU Case Study)

The Genoil GHU (Hydroconversion Upgrader) technology is positioned in the market as a modular solution for the deep upgrading of heavy oil directly at the field.

2.1. Chemical Transformation Mechanism

Unlike classic atmospheric-vacuum distillation units, the GHU unit operates on the principle of high-temperature hydrogenation under supercritical pressure (up to 180–200 atm).

- Macromolecule Destruction: Long hydrocarbon chains of heavy fractions are split in the presence of a catalyst.

- Hydrogenation: Hydrogen instantly embeds into the formed carbon bond ruptures. While traditional thermal coking inevitably loses commercial raw material mass (turning into coke), hydroconversion ensures an absolute increase in commercial mass due to the physical weight of the added hydrogen.

2.2. Reactor Block Architecture

The technology developers rely on a stationary catalyst bed (Fixed-Bed).

Engineering Vulnerability: The main technological risk lies in this architectural solution. Heavy oil is characterized by an extreme concentration of asphaltenes and metals (vanadium, nickel) that irreversibly deposit on the stationary catalyst, causing its rapid deactivation and a critical rise in hydraulic resistance. At a remote field, this necessitates regular system shutdowns to reload the expensive catalyst.

2.3. Metallurgical Barrier and Hydrogen Embrittlement

When evaluating the life cycle of GHU-class technologies, it is necessary to consider a systemic barrier ignored in investment teasers:

- Hydrogen Corrosion: At high temperatures and extreme pressure, atomic hydrogen diffuses into the crystal lattice of steel, causing irreversible "hydrogen embrittlement". This dictates the absolute necessity of using specialized grades of high-alloy steel with chromium and molybdenum additives.

- Technological Sovereignty: In the current geopolitical realities, access to Western large-tonnage forgings is blocked. The project's viability critically depends on strategic cooperation with domestic heavy machinery manufacturing.

CHAPTER III. Global Technological Landscape

To make balanced macroeconomic decisions, one must objectively assess the position of independent vendors on the global hydroprocessing technology map.

| Technology | Vendor / Holder | Operating Principle | Current Status (2026) | Geopolitical Availability |

|---|---|---|---|---|

| EST | Eni (Italy) | Slurry Bed | Global benchmark. 99.9% conversion. | Blocked by sanctions |

| LC-FINING | Chevron (USA) | Ebullated-bed | Industrial standard. | Unavailable to the RF |

| Uniflex | Honeywell UOP | Slurry Bed | Maximum yield of light fractions. | Unavailable to the RF |

| VCC | KBR (USA/Germany) | Combi-cracking | Operating at the TANECO complex. | Service maintenance risks |

| Genoil GHU | Genoil (Canada) | Fixed-bed | Pilot projects. | High (venture stage) |

CHAPTER IV. The Russian Path: Sovereignty at the Nanoscale

The Russian Federation possesses an advanced scientific school of slurry hydrocracking (based at the Topchiev Institute of Petrochemical Synthesis, TIPS RAS), capable of offering a full-fledged sovereign alternative to foreign licenses.

- Essence of the Innovation: Abandonment of vulnerable stationary beds in favor of nanocatalysts continuously circulating in the reactor in a single stream with the oil. This allows efficient conversion of feedstocks of any complexity profile (including natural bitumens).

- Industrial Reference: The operation of the project at the TANECO facility proves that domestic technologies actually surpass the theoretical performance of foreign analogs in terms of actual refining depth.

4.1. Hardware Audit: The Import Substitution "Traffic Light"

The creation of sovereign Upstream Refining complexes must rely on the actual production capabilities of domestic industry:

| Critical Unit Component | Status in the RF | Key Manufacturers / Solutions |

|---|---|---|

| Hydroprocessing Catalysts | High Readiness | Gazpromneft-Catalytic Systems, RN-Kat, TIPS RAS. The base market need is securely covered by proprietary developments. |

| High-Pressure Reactors (up to 200 atm) | Limited (Queues) | Competencies in thick-walled forgings are preserved (Uralhimmash, Atomenergomash), but production capacities are contracted for years ahead. |

| Pumps for Hot Slurries (Slurry) | Medium Readiness | HMS Group enterprises. Active testing of seals for abrasive media (replacing products of departed Western vendors) is underway. |

| Hydrogen Reciprocating Compressors | Critical Vulnerability | Historical dependence on imports (Ariel). Accelerated scaling of production by Kazancompressormash and the Borets plant is required. |

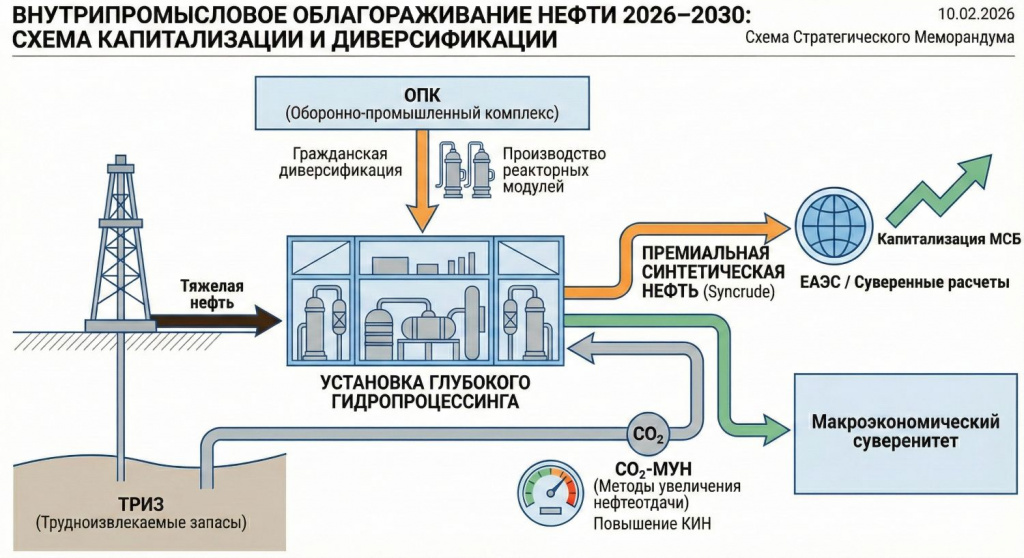

4.2. Solution Package: State Order for the Defense-Industrial Complex (Technological Mobilization)

The critical bottlenecks of hydroconversion units are thick-walled ultra-high-pressure reactors and compressor stations. This nomenclature is technologically identical to equipment produced for the nuclear submarine fleet and the aerospace industry.

BREAKTHROUGH SOLUTION — The "Counter-Conversion" Mechanism: It is proposed to initiate a mechanism for loading reserve and partially idle capacities of the Defense-Industrial Complex (DIC), specializing in high-alloy steels and precision mechanics, with the serial production of large-tonnage civilian Upstream Refining modules.

- Economic Impact: Formation of a long-term, high-margin order for DIC enterprises, ensuring the diversification of financial flows without compromising the execution of the State Defense Order (SDO).

- Technological Sovereignty: Critical dual-use competencies (protecting alloys from hydrogen embrittlement, cryogenics, ultra-high-pressure operations) are scaled and capitalized on the commercial market.

- Accelerated Launch: The deployment of sovereign oil refining capacities is reduced from 7–10 to 3–4 years by relying on the active machine park and engineering reserve of the military-industrial complex. Investments in the fuel and energy complex become direct investments in preserving the human capital of the defense industry.

CHAPTER V. Economics of Hydrogen Consumption and Energy Security

5.1. Hydrogen Index: Mass Balance

For the deep conversion of 1 barrel of heavy oil residue into high-quality synthetic crude (Syncrude), a calculated volume of pure hydrogen is required — on average from 2 to 4 kg of H₂. Industrial modes necessitate the mandatory design of a dedicated make-up gas loop and continuous purge, which predetermines the high capital intensity of the complex.

5.2. Cost of the Molecular Basis

| Hydrogen Type | Production Technology | H₂ Cost per 1 Bbl. | Economic Viability |

|---|---|---|---|

| Gray (from natural gas) | Steam Methane Reforming (SMR) | ~$5 – $7 | High. Optimal and profitable path in RF realities. |

| Blue (with CO₂ capture) | From gas + CO₂ capture | ~$8 – $12 | Medium. Justified exclusively with targeted subsidies. |

| Green (from renewables) | Electrolysis (RES) | ~$14 – $25 | Low. Prohibitively expensive for oil refining processes. |

5.3. Autonomy vs. Infrastructural Integration

Ensuring the stable operation of an upgrading complex with a capacity of 1 million tons of raw materials per year requires building a hydrogen generation station comparable in scale to a full-fledged chemical plant. This fact shifts the initiative from localized modernization into the class of large-scale infrastructure construction.

5.4. Monetization of APG (Flaring)

Subsoil users in the Russian Federation have a strategic advantage over the EU — the ability to deeply process associated petroleum gas (APG) directly at the fields.

- Transforming Ecology into Profit: Instead of paying penalties for APG flaring, the operator converts the gas into an efficient chemical reagent (H₂) for its own technological cycle.

- Logistical Optimization: In-field production of light Syncrude neutralizes infrastructure constraints, allowing year-round shipment via standard unheated pipelines.

5.5. Practical Case: Bypassing Transneft's "Quality Bank"

Economics of Double Benefit: The specifics of the Russian pipeline monopoly create a massive hidden premium for in-field upgrading. Companies (especially in the Volga-Ural province) are forced to deliver high-sulfur raw materials into the trunk pipeline, which incurs a hidden discount under the "Quality Bank" settlement mechanism.

A hydroconversion unit at the wellhead transforms ballast into premium low-sulfur Syncrude. The enterprise not only gets rid of systematic deductions but also starts receiving compensation premiums from other shippers for improving quality metrics in the pipeline flow. Simultaneously, operational expenses for purchasing light condensate for dilution drop to zero.

CHAPTER VI. Impact on the Mineral Resource Base (SRC and ORF)

At the macroeconomic level of state planning, the effect of in-field hydroconversion lies not in the mechanical refining of raw materials, but in the direct capitalization of the subsoil through two fundamental factors: a multiple increase in production marketability and the formation of an economically viable contour for Enhanced Oil Recovery (EOR) methods.

It is important to establish a strict methodological boundary: in-field upgrading does not increase the Oil Recovery Factor (ORF) on its own. The ORF increases solely due to physical and chemical impact on the productive reservoir.

6.1. Reserves Reclassification: From Low-Liquidity Resource to Industrial Asset

The implementation of in-field upgrading complexes shifts the economic boundary of recoverability. What was previously classified as Hard-to-Recover Reserves (HTRR) or off-balance volumes—due to quality discounts, dilution costs, transport seasonality, and infrastructure constraints—becomes industrially profitable by improving the commercial characteristics of the flow right at the field.

The practical meaning for State Reserves Commission (SRC) registries is as follows:

- The profitability threshold for involving viscous and high-sulfur fractions is lowered.

- Dependence on imported diluents and their complex logistics is reduced.

- The stability of product quality increases, simplifying sales and removing a portion of penalty deductions.

- It becomes possible to project-justify the transfer of some reserves from contingent categories to industrially developed ones due to a radical improvement in the economic indicators of development.

Critical Methodological Caveat: The upgrading unit itself is not a legitimate basis for a mechanical "category upgrade" of reserves. The fundamental basis is a confirmed technological development scheme with recalculated economics, a feasibility study, and engineering solutions for production and infrastructure.

6.2. Synergy with Enhanced Oil Recovery (EOR) Methods

Hydrogen production for deep hydroconversion, if organized at the field or within a cluster, forms a concentrated CO₂ stream. With capture and compression, this stream can be directed into the reservoir pressure maintenance system and used as a working fluid to enhance oil recovery.

The synergy's purpose is not ecological or declarative, but strictly engineering and economic: a byproduct of hydrogen infrastructure turns into a resource for production. Actual mechanisms of CO₂ impact on the reservoir:

- Reducing oil viscosity by dissolving CO₂.

- Improving displacement by lowering interfacial tension.

- Increasing sweep efficiency with properly selected regimes and mobility control.

- The potential for multiplying the effect upon reaching Miscible displacement conditions for CO₂ and oil.

Technological Barrier and Risk Management: Without mobility control, CO₂ is prone to breakthrough via high-permeability channels. A viable project must include sweep-leveling regimes, such as water-alternating-gas (WAG), foam systems, injectivity profile treatments, and the isolation of breakthrough intervals.

6.3. ORF Increase as an Effect of the "Upgrading + CO₂-EOR" Contour

The ORF increases only through impact on the reservoir. In-field hydroconversion and upgrading are situated downstream of the wellhead (on the surface) and do not directly change the ORF. Their role in ORF growth is indirect and consists of two channels:

- The Financial Channel: Upgrading increases the project's Netback, reduces operational losses on quality and transport, and creates a stable funding source for EOR measures, which often fail to reach threshold profitability without this added margin.

- The Technological Channel: Hydrogen infrastructure, when coupled with capture, forms a CO₂ stream for injection, thereby providing a material resource for CO₂-EOR as a direct mechanism for increasing oil recovery.

A correct definition of target ORF indicators should be scenario-based, rather than a unified "one figure for all". For mature provinces, it is reasonable to set the following ranges:

- Base Scenario: ORF growth of 0.05–0.12 due to the implementation of CO₂-EOR under standard reservoir and infrastructure constraints.

- Improved Scenario: ORF growth of 0.12–0.20 given confirmed miscibility achievability, sufficient pressure, strict mobility control, and an appropriate well spacing.

- Upper Limit (0.50–0.55): Permissible only as a rare exception and must be strictly justified by calculations, 3D modeling, and pilot test results, rather than just being stated in the text.

Thus, the correct doctrinal thesis is not "upgrading increases the ORF", but rather "upgrading makes the EOR loop, which increases the ORF, economically and infrastructurally feasible".

6.4. Reproduction of the Mineral Resource Base at the Nanoscale

The paradigm of mineral resource base (MRB) reproduction is shifting from an extensive model to the management of already tapped assets through precise physical, chemical, and hydrodynamic impact on the reservoir. For the state, this means a systemic transition from chasing new licenses to improving recoverability and extending the life of mature provinces.

From a practical standpoint, MRB reproduction here is ensured by:

- Involving previously unprofitable volumes by improving the marketability and economics of production.

- Increasing ultimate recoverability through the justified application of EOR.

- Enhancing the reliability of design solutions by accumulating field regime data and their digital verification.

6.5. Geography of Application: Top 3 Priority Clusters in the Russian Federation

| RF Macroregion | Typical Assets | Problem as an Operational Liability | Solution as Asset Synergy |

|---|---|---|---|

| Timan-Pechora (Komi) | Yaregskoye, Usinskoye, and similar heavy oil profiles | High viscosity, expensive treatment and transport, critical dependence on diluents. | In-field upgrading to obtain a more transportable flow + economic backing for thermal and gas EOR methods. |

| Volga-Ural (Volga Region) | Assets of Tatarstan, Bashkortostan, Samara Region, and other high-sulfur oils | High sulfur content, quality discounts, difficulty bringing raw materials up to market requirements. | In-field upgrading to remove discounts + clustered hydrogen infrastructure; with CO₂ capture — a resource for CO₂-EOR and pressure maintenance. |

| Arctic Cluster | Vankor block, Vostok Oil, and similar projects | Expensive logistics, transport limitations, penalties and losses from APG. | Converting APG into hydrogen for the technological cycle + obtaining a stable transportable product; with capture — CO₂ as a resource for EOR at local facilities. |

6.6. Policy Package: SRC Institutional Lift (Accelerated Capitalization of Hard-to-Recover Reserves)

The methodological vulnerability of previous regulatory discourse lay in the attempt to tie a multiplying coefficient to the mere presence of an upgrading unit. This is methodologically weak: a downstream unit is not proof of increased oil recovery. A workable scheme must tie multiplying factors to a confirmed reservoir impact contour and its level of proof.

BREAKTHROUGH SOLUTION: It is proposed to approve, at the level of the Ministry of Natural Resources and the State Reserves Commission (SRC), a methodology for confirmed technological efficiency with a tiered scale.

1. Condition of Application:

The Technological Efficiency Coefficient (TEC) is applied only if there is a project contour affecting the reservoir. Approved EOR design solutions are required, including the source and preparation of the injection agent, injection scheme, monitoring, mass balances, and economic model.

2. Tiered TEC Scale by Proof Level:

- Design readiness level: Approved design documentation and infrastructure plan exist (the coefficient has a limited status).

- Pilot level: Pilot field tests have been conducted with measurable production gains and confirmed process controllability (elevated coefficient).

- Commercial rollout level: Repeatability of the effect across multiple zones is confirmed, and stable operation and monitoring are established (maximum coefficient on the scale).

* It is advisable to set numerical values of the coefficients as a range and link them to the asset type, rather than fixing a single number for all.

3. Legal Basis for Changing Reserve Status:

The basis is not the commissioning certificate of the upgrading unit, but a set of documents confirming the reservoir impact contour: modeling results, pilot program and outcomes, monitoring, mass balances for the injection agent, and actual dynamics of production rates and water cut.

4. Monetization and Funding Mechanism:

The state capitalizes not on the fact of equipment acquisition, but on the confirmed increase in recoverability and profitability. This allows for:

- justifiably increasing the value of recoverable reserves on the company's balance sheet;

- forming a solid collateral base for project financing;

- moving assets from a chronically underinvested category to one with a clear technological and financial risk profile.

CHAPTER VII. Due Diligence Checklist: Questions for Licensors

At the pre-investment stage, the client must obtain exhaustive engineering guarantees from technology developers on the following points:

- Mass Balance: Guaranteed H₂ consumption per 1 barrel of specified Russian crude.

- Catalyst Lifespan: Turnaround run without regeneration at heavy metal contents in the feed exceeding 200 ppm.

- EPC Contract Feasibility: Documented confirmation of reactor supply logistics chains under active sanction regimes.

- Syncrude Stability: Confirmation of aggregative stability (guarantee of preventing asphaltene precipitation during transport via the Transneft PJSC system).

CHAPTER VIII. Project Economics and Funding Architecture

8.1. Base Economic Model and the Impact of the Central Bank Rate

For a standard unit with a capacity of 2 million tons of feed per year, total CAPEX is estimated at $650 million. The projected EBITDA of the complex with an $18/barrel spread is ~$190 million/year. However, the cost of servicing debt capital critically determines the investment viability of real-sector projects:

| CBR Rate | Effective Loan Rate | Payback Period (PBP) | NPV (10-year horizon) |

|---|---|---|---|

| 8% (Target) | 10% | 4.2 years | + $410 million |

| 16% (Tight) | 18% | 6.8 years | + $120 million |

| 21% (Critical) | 23% | Investment insolvency | - $15 million |

8.2. Policy Package: Tax Maneuver 3.0 ("Reverse Excise on Destruction")

Since 2019, the Russian Federation has successfully applied the "reverse excise" (damper) mechanism, which stimulates the production of commercial gasoline. To force the launch of the hydrogen transformation, it is proposed to institutionally extend this fiscal logic to the processes of deep utilization (destruction) of heavy oil residues.

- Mechanism Essence: For every ton of vacuum resid or high-sulfur fuel oil fed to the hydroconversion block and physically transformed into Syncrude or light fractions, the operator receives a direct targeted tax deduction from the Mineral Extraction Tax (MET) or Additional Income Tax (AIT).

- Progressive Scale: The subsidy size is strictly tied to the achieved depth of refining: the more radical the carbon conversion (residue-free), the higher the deduction rate applied.

- Macroeconomic Meaning: The state grants the corporation a direct preference for physically not producing low-margin and toxic fuel oil. For the macroeconomic balance of the federal budget, this fiscal tool is mathematically more profitable than the regular shortfall in customs duties (due to discounts on heavy crude) and the artificial subsidization of Russian Railways (RZD) logistics for fuel oil exports.

8.3. Financial Navigator: Anti-Crisis Arsenal of State Support

Under the conditions of maintaining a prohibitive key rate by the CBR, the implementation of capital-intensive Upstream Refining projects exclusively by the commercial sector is impossible. Projects are viable only through state co-financing mechanisms:

- Transition to AIT: Transferring assets to the Additional Income Tax (AIT) regime, where fiscal withdrawal is made from the financial result of selling a premium product, rather than from the physical volume of extracted high-carbon liquid.

- Cluster Investment Platform (CIP): A mechanism by the Ministry of Industry and Trade of the Russian Federation for funding priority import-substitution projects at a preferential subsidized rate (30% of the CBR key rate + 3 p.p.).

- Project Finance Factory (VEB.RF): An interest rate risk hedging mechanism. The development institute fixes the base rate for the borrower, and all excesses of the "key rate" are compensated to syndicate banks directly from the federal budget.

CHAPTER IX. Global Market and EAEU Strategy

9.1. Asian Technological Dictate and the "Eurasian Standard"

Global power centers (China, India) have completed the formation of sovereign hydrogen hubs. Corporations on the level of Sinopec and Reliance function as technological absorbers, purchasing Russian hydrocarbons at maximum discount and leaving 100% of the value added within their economies. If the status quo continues, Russia risks cementing itself in the role of a passive raw material donor.

An asymmetrical response must be the introduction of a new standardized commodity to the global market — Eurasian Syncrude. Its legal classification as a product of high-tech refining exempts the asset from several sanction restrictions imposed exclusively on raw, unprocessed crude oil.

9.2. Policy Package: Industrial Proving Ground (Integration of Russian and Belarusian Petrochemical Assets)

Key oil refining facilities of the Republic of Belarus (Mozyr Oil Refinery, Naftan JSC) in the current geo-economic environment are forced to operate in a low-margin tolling processing regime. It is strategically viable to transform these sites into the first integrated Eurasian hub for Eurasian Syncrude production.

- Feedstock Routing: Targeted redirection of high-sulfur oil flows from the RF to Belarusian sites under special long-term Union State tariffs.

- Technology Transfer: Large-scale deployment of sovereign nano-slurry hydrocracking units (based on TIPS RAS technologies) at Belarusian refineries. Belarusian industry receives cutting-edge technology; the RF gets a reliable proving ground for industrial scaling.

- Export Breakthrough: Production of high-margin middle distillates (jet fuel, Euro-6 diesel) with subsequent export through the Baltic port infrastructure of the RF (Ust-Luga) under a unified brand. This turns the Union State from a logistics transit hub into a sovereign market maker in the global energy market.

9.3. Policy Package: Sovereign Settlement Contour (Digital Commodity Clearing Platform)

The approval of the Eurasian Syncrude macro-regional standard opens a historic window of opportunity for reforming the monetary and financial architecture (in line with the concepts of EAEU integration and BRICS de-dollarization).

BREAKTHROUGH SOLUTION: The "Digital Energy Asset (DEA)" Strategy

Creating an independent digital commodity distribution platform based on specialized EAEU exchanges. Energy supply settlements are moved to a secure digital contour, where the tokenized Eurasian Commodity-Energy Standard (ECES) serves as the unit of account.

- Backing Mechanism: The digital unit (token) is issued strictly against the confirmed physical volume of shipped synthetic raw material and is strictly hedged by a basket of liquid basic resources of Eurasia (energy, hydrocarbons, gold, grain).

- Escaping the Fiat "Scissors": The platform's goal is to completely neutralize transaction costs, sanction risks, and cross-currency volatility (dependence on the dollar and yuan). The value of the payment instrument is pegged to fundamental demand for actual physical energy.

- Macroeconomic Paradigm Shift: Russia and its allies stop selling strategic wealth for inflationary third-country currencies. A transition is made to exporting advanced technologies and energy in exchange for a sovereign digital asset, 100% backed by a real industrial basis.

CONCLUSION: Strategic Verdict and the New Russian Doctrine

Maintaining the inertial paradigm of exporting crude oil leads to the irreversible technological depletion of the fuel and energy complex. The industry is caught in the "technological scissors" between Western license blocking and Eastern price dictates from monopoly buyers. The core of the new doctrine must be the alternative-free transition to a sovereign Upstream Refining model.

Russia operates with a fundamental asset inaccessible to competitors — a massive surplus of cheap power generation. The symbiosis of available nuclear and hydroelectric power capacities allows for collapsing the cost of technological hydrogen production to an unprecedented $1.2–3.5 per kilogram.

SUMMARY

The implementation of the macro-regional Eurasian Syncrude standard paired with digital commodity clearing goes far beyond private corporate modernization. It is a large-scale transformation of the state's economic paradigm. The industrial conversion of ultra-cheap megawatt-hours and high-carbon feedstocks into a clean, high-margin energy carrier turns Russia into a global "energy offshore".

By monetizing unmatched national advantages in baseline generation and DIC competencies, the Russian Federation sheds its status as a passive raw material donor. The state assumes the role of a global technological leader, seizing a historic chance to dictate the architecture and operating rules of markets in the realities of the sixth technological paradigm.

IMPLEMENTATION ROADMAP (2026–2030)

Stage 1: Institutional Launch (2026)

- The "Sovereign Hydrocracking" Consortium: Integration of the competencies of TIPS RAS (scientific base), Rosatom State Corporation (hydrogen generation), DIC enterprises (reactor modules), and VIOCs (HTRR resource base).

- Launch of Commodity Clearing: Development of the Digital Energy Asset (DEA) architecture under the auspices of the macroeconomic structures of the Union State and the EAEU.

Stage 2: Technological Scaling (2027–2028)

- Launch of Pilot Proving Grounds: Testing industrial regimes in the "Volga-Hydrogen" cluster and integration with facilities of the Republic of Belarus.

- Tax Maneuver 3.0: Approval of the tiered TEC methodology in the SRC reserve classification and launch of the "Reverse Excise on Destruction" mechanism.

Stage 3: Formation of a New Global Market (2029–2030)

- Administrative Export Filter: Phased increase of export duties on fuel oil and heavy unprocessed oil to prohibitive levels.

- Listing of Eurasian Syncrude: Full launch of trading for the new benchmark with settlements in the sovereign clearing contour.